Related: $10 AI Medical Stock Landing Massive Contracts!

This week, we’ll review a company that several of you asked me to put through The Value Meter. It’s a holding company owned by one of the world’s wealthiest and most successful investors.

Founded in 1987, Icahn Enterprises (Nasdaq: IEP) is majority-owned by billionaire investor Carl Icahn and his son, Brett Icahn. Shares of the company provide investors with exposure to Carl Icahn’s personal investment portfolio, which consists of public and private companies across a wide variety of industries – ranging from oil and gas to real estate.

Over the past several months, shares have fallen drastically, dropping as much as 65% from a 52-week high to a nearly 20-year low.

What was the catalyst for the collapse?

Last May, short seller Hindenburg Research released a scathing report on Icahn Enterprises. It claimed that the company was overleveraged, overvalued and paying out its fat dividends using money from new investors rather than its cash flows.

Naturally, the report scared investors, and it sent shares plummeting 20% the day it was published. A few months later, the company ended up slashing its dividend in half, pushing share prices down even further.

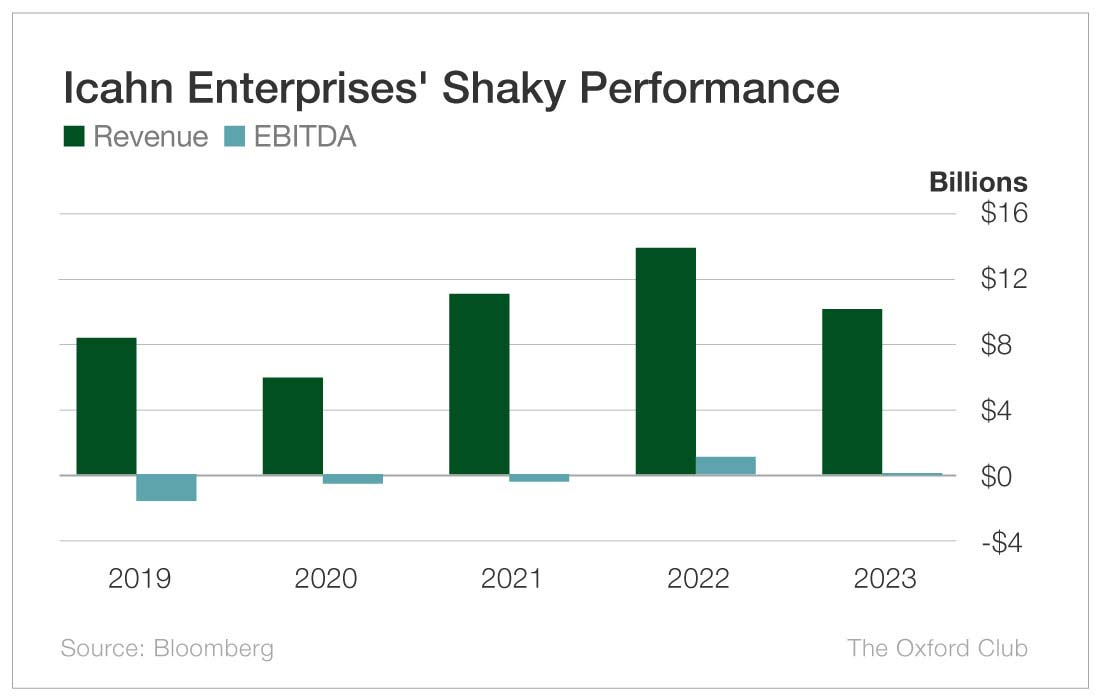

To add insult to injury, the company just announced a sharp decline in revenues in 2023 as well as an earnings loss, which is sure to discourage investors even more.

In short, the company’s shareholders have had a really tough year.

Icahn Enterprises’ revenues have tended to fluctuate over the past several years, and profitability (as measured by EBITDA, or earnings before interest, taxes, depreciation and amortization) has been inconsistent.

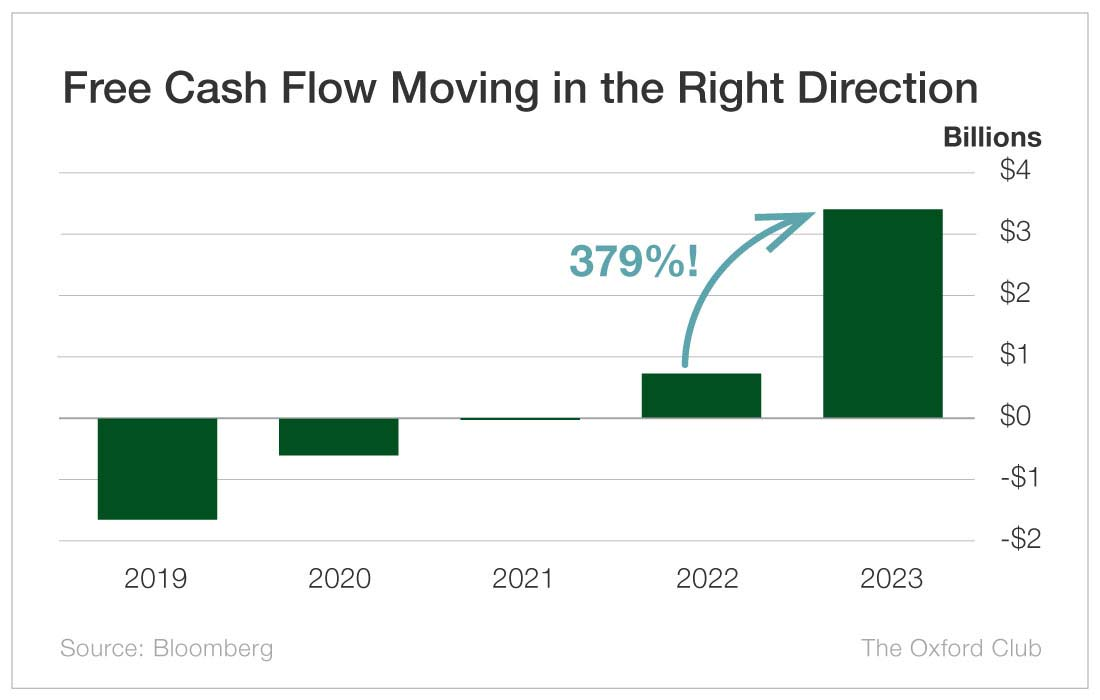

But the company’s free cash flows have been in a strong uptrend in recent years.

Free cash flows reached a whopping $3.4 billion in 2023, up 379% from $717 million in 2022 and up 21,356% from $16 million in 2021.

Among the more than 3,600 stocks scanned by my updated system – which I introduced in last week’s Value Meter – Icahn Enterprises falls between one and two standard deviations above the average. (Remember, the higher a stock’s ranking, the more undervalued it’s likely to be.)

The ratio of the company’s enterprise value to its net assets, or its EV/NAV ratio, is about 1.4. That means its acquisition cost is only 40% above its net asset value. (An EV/NAV ratio of 1.4 is about one-fourth of the average for all eligible stocks that were screened – that is, stocks with positive cash flows and net assets.)

Plus, Icahn Enterprises’ trailing 12-month free cash flow was an average of 32% of its net assets over the past two quarters, compared with an average of 26% among eligible companies. In other words, it generates more cash from its assets than most companies would.

Overall, the stock appears to have been beaten down too harshly.

Icahn Enterprises represents a very diverse investment portfolio with stakes in businesses across nearly every industry. While it’s not quite a high-flying growth stock, its sizable free cash flow growth in recent years shouldn’t be ignored – especially at today’s market prices.

The Value Meter rates shares of Icahn Enterprises as being “Slightly Undervalued.”

EV charging stations that pay you up to $93/day!

Our government just realized it can't meet its 2030 climate targets without outside help…

And it's created a major income opportunity for average Americans.

Specifically, the White House is channeling $7.5 billion of “backdoor” infrastructure funding to a tiny clique of “special companies”…

Companies that have been tasked with installing and running 450,000 new electric vehicle charging stations along our roads and highways.

And that's fantastic news for you…

Because not only are these special companies set to rake in $563 million in profit this year alone…

They're also required to share ALL of that cash with ordinary Americans.

If you know how to grab a slice of this new income stream…

It could be the easiest money you ever make.